Startup failures rarely come down to a single cause. But they do follow patterns.

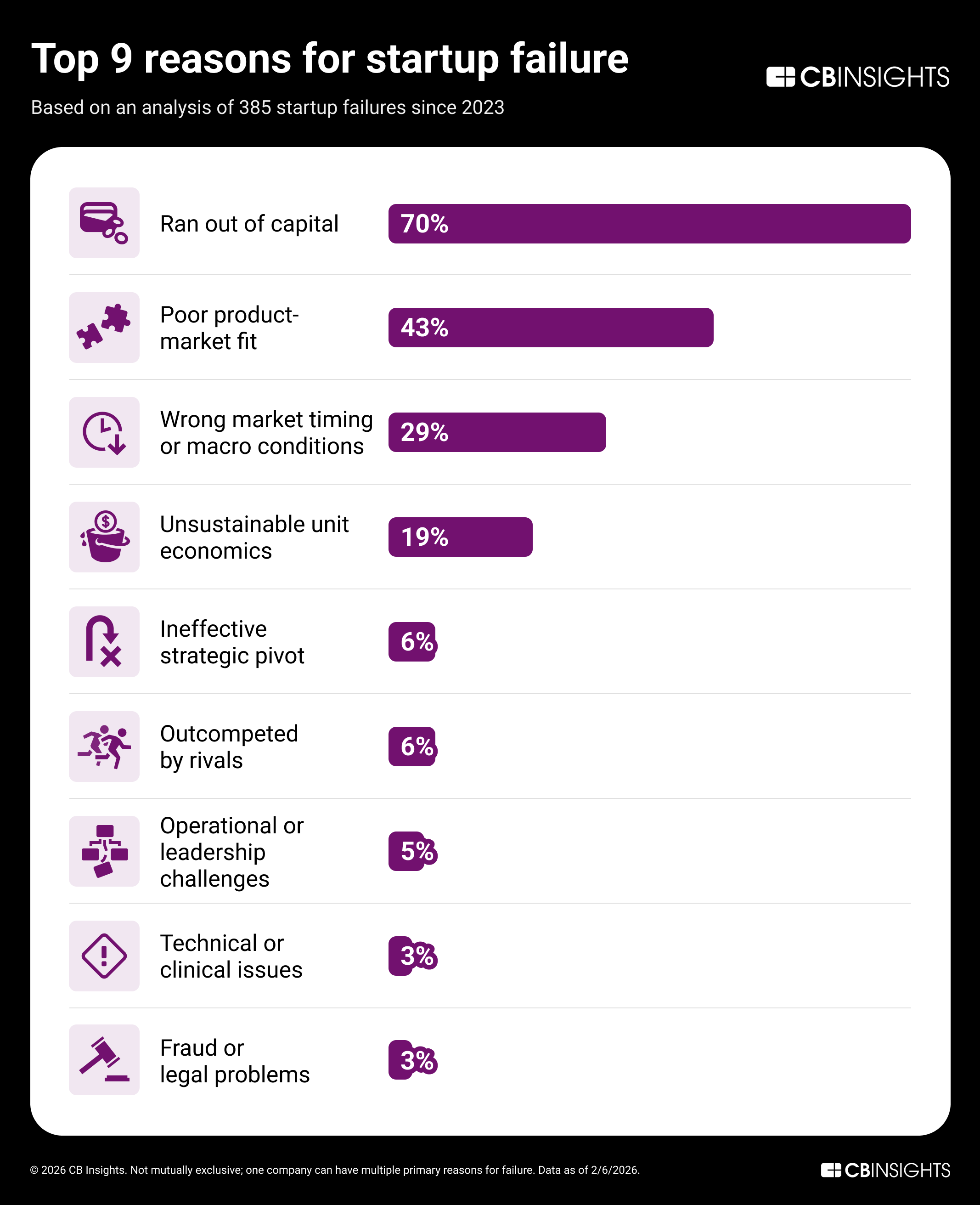

We analyzed public post-mortems, founder interviews, and shutdown announcements from 431 VC-backed companies that shut down since 2023 in the post-zero-interest-rate shakeout. “Ran out of capital” tops the list at 70%, but it’s almost always the final cause of death, not the root problem.

Here’s what CB Insights data shows.

Why do startups fail?

Capital running out is where these stories end. The more telling causes — poor product-market fit (43%), bad timing (29%), and unsustainable unit economics (19%) — reveal why the capital dried up in the first place.

Since many startups cited multiple reasons for their failure, the chart below exceeds 100%. The analysis includes 385 companies for which failure reasons could be identified.

Two-thirds of product-market fit (PMF) failures were early-stage companies that never found a market. But 20 Series B+ companies also cited poor PMF as a primary cause. Those later-stage companies raised on early traction that never widened into a real market. Zume ($446M, Series C), which pivoted from robot-made pizza to sustainable packaging and still failed to find a viable market, is one example.

Bad timing or macro conditions drove a disproportionate share of failures in climate & energy, food & agriculture, and blockchain. These sectors attracted heavy capital in 2021-2022 on trends that never materialized. For example, New Age Meats ($32M) and RECUR ($55M) raised at the peak of the alt-protein and NFT waves respectively, and both shut down when the market didn’t follow through.

How we built this report

Using the CB Insights platform, we identified 431 VC-backed startups that publicly shut down since 2023, excluding companies that had a prior exit. We then categorized the companies (with sufficient data) by primary reasons for failure. Then, we leveraged CBI signals, such as Mosaic health & potential scores and business relationships, to surface key patterns across the cohort.

What are the warning signs?

While founders cite a range of causes in shutdown post-mortems, CB Insights’ predictive signals show measurable deterioration in company health and activity in the months leading up to shutdown.

Mosaic declines: CB Insights’ Mosaic score, a proprietary measure of private company health and potential scored 0 to 1,000, shows a deterioration curve in dead companies. Among companies with full 12-month Mosaic data, 72% saw their score decline in the year before death, with scores dropping by 15% on average.

Partnership fall-off: Among the 206 companies (48%) with any tracked business relationships, partnership activity was notably front-loaded and thinned as companies approached shutdown, dropping 44% from 12-24 months before death to the final 12 months.

Shrinking headcounts: Among companies with headcount data, two-thirds were shrinking in the 6 months before death. Nearly a third died with 10 or fewer employees. About 15% died with over 100.

How much runway do startups really have?

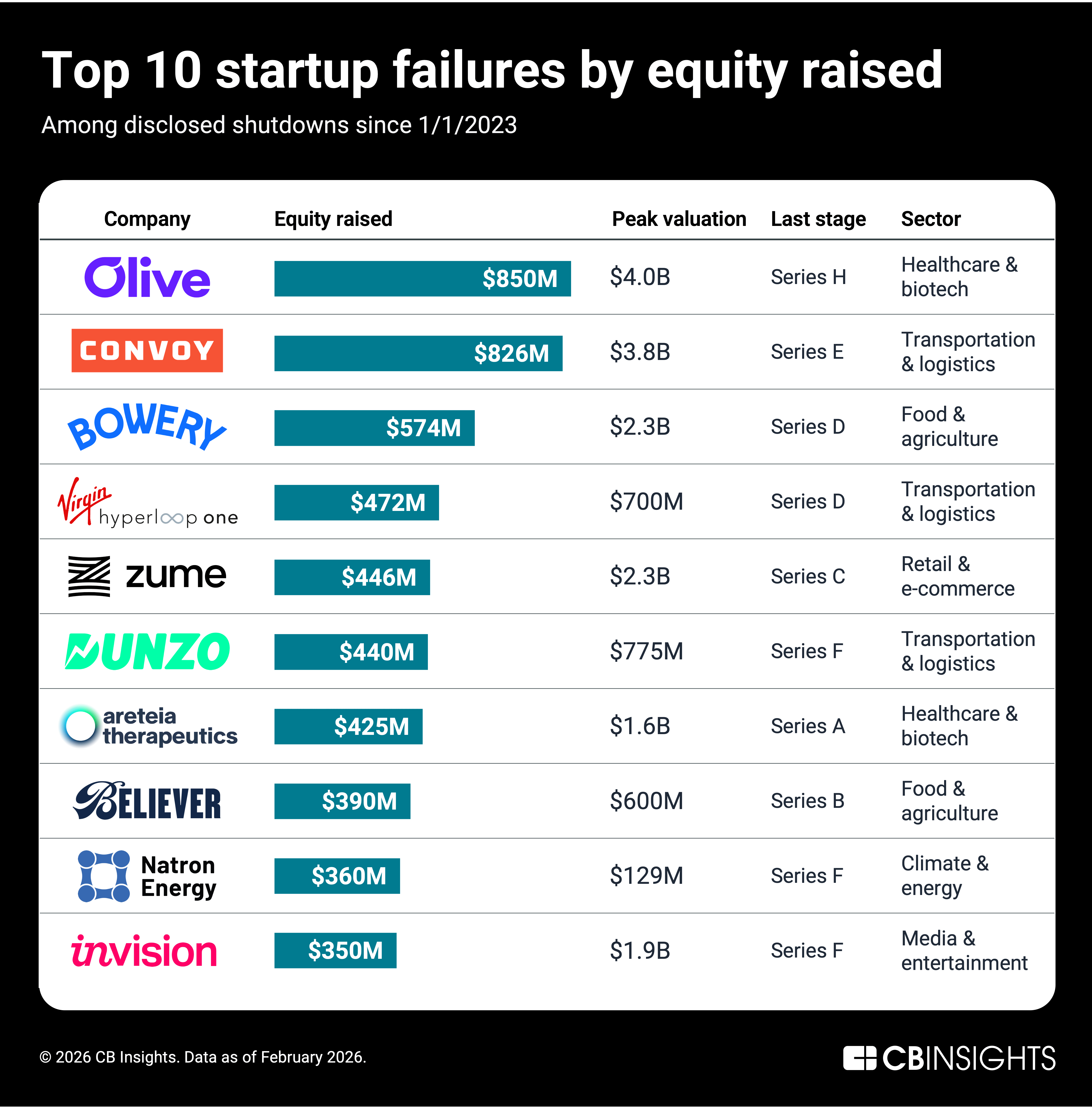

Money can’t save you: The 431 companies in this analysis raised a combined $17.5B in equity funding before dying. The median company raised $11M and the average was $48M, pulled up by a long tail of heavily funded failures. Topping the chart with nearly $1B raised in funding are healthcare AI automation startup Olive and digital freight brokerage Convoy. Both hit ~$4B valuations during pandemic-era booms — and both shut down within two weeks of each other in October 2023 as their markets turned.

Funding cliff: The median time from last fundraise to death is 22 months. In other words, over half of the companies in our dataset died within 2 years of their last raise. However, nearly a quarter of startups had been “walking dead” for over 3 years since their last raise before officially going under. Currently, there are nearly 50,000 VC-backed startups that haven’t raised funding since the start of 2023.

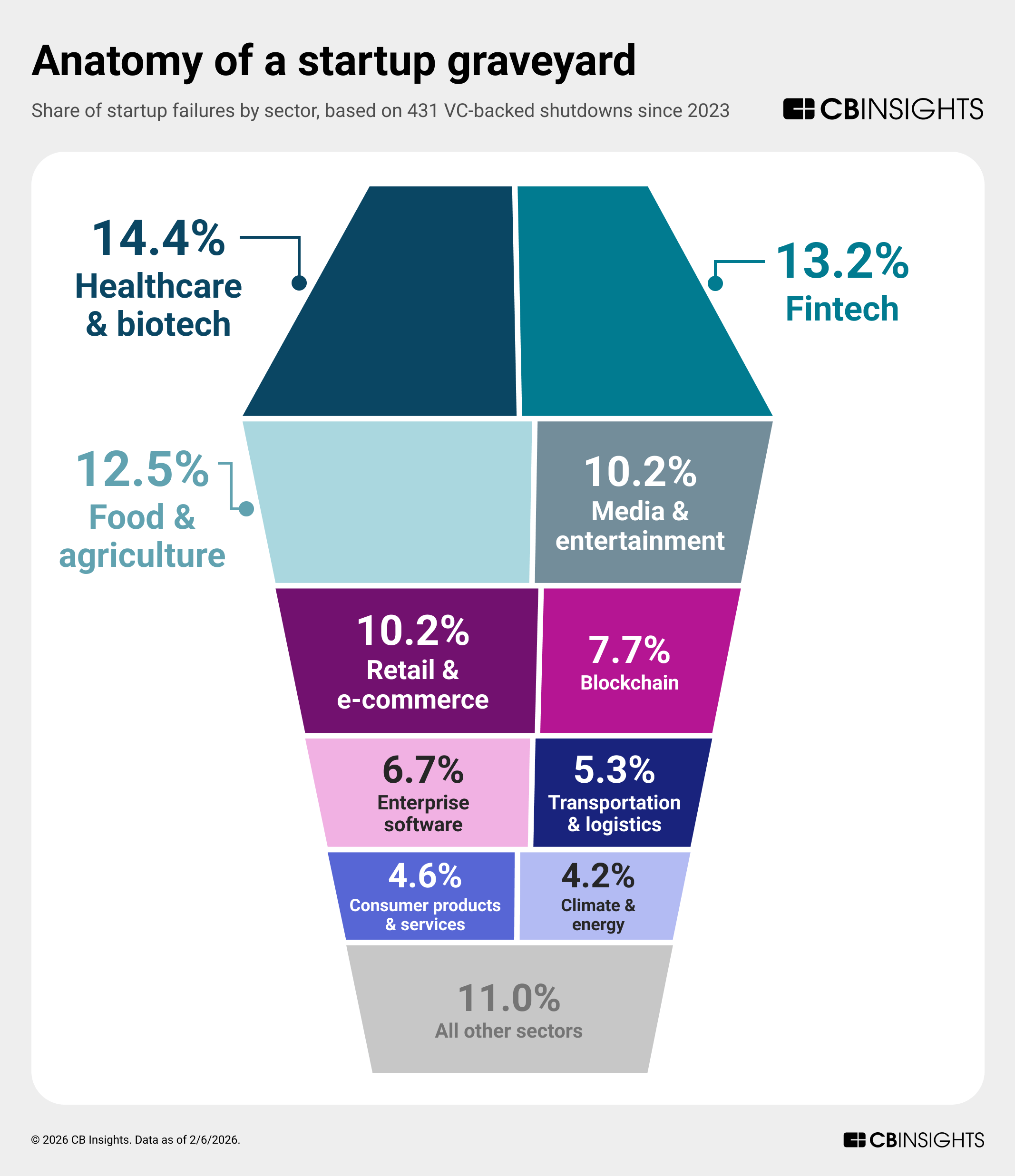

Which sectors account for the most failures?

Healthcare & biotech (62 companies, 14%) leads in both failure count and capital destroyed ($5.1B). The funding total was buoyed by biotech companies (over half of the category), reflecting the capital intensity of clinical-stage drug development. For example, Areteia Therapeutics raised $425M but shut down after its respiratory therapeutics for asthma didn’t meet expectations in clinical trials.

Fintech (57 companies, 13%) ranks second by count but the failures skew early-stage: median equity funding of just $4M, below the dataset-wide median of $11M and a fraction of healthcare’s $47M. 60% of the failures were based outside of the US (vs. 47% of the full dataset), including in emerging markets across Africa, India, and Southeast Asia. High-profile examples such as ZestMoney ($114M equity funding) and Ula ($141M) highlight the 2021-2022 emerging-market fintech funding boom, which produced companies that struggled with unit economics as capital dried up.

Food & agriculture (54 companies, 13%) is the more surprising entrant. Roughly a third of these are alt-protein or cultivated meat startups like Believer Meats ($390M raised) and Motif FoodWorks ($344M), pointing to a broader unwinding of the alternative protein wave.

If you aren’t already a client, sign up for a free trial to learn more about our platform.